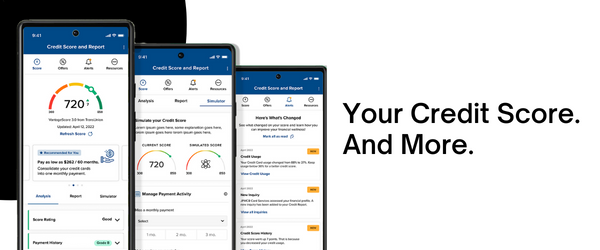

STAYING ON TOP OF YOUR CREDIT HAS NEVER BEEN EASIER

With one powerful tool, access your credit score, full credit report, credit monitoring, financial tips and education.

You can do this ANYTIME and ANYWHERE and for FREE.

BENEFITS OF CREDIT SCORE:

- Daily Access to your Credit Score

- Real-Time Credit Monitoring Alerts

- Credit Score Simulator

- Personalized Credit Report

- Special Credit Offers

- Financial Checkup with Wellness Score

- And More!

The benefits are endless, so there is no need to wait. Access your credit score and report through Anytime Online and our mobile app, brought to you by SavvyMoney.

Please note, there are many different credit scores and scoring models available. Your credit score provided through this complimentary service may use a different scoring model than lenders. Your score may differ when applying for a loan from a financial institution.

FAQs

Any institution that lends money – credit unions, banks, credit card companies, financing companies, mortgage lenders, and others – can use a credit score to help them assess whether you meet their lending criteria. These institutions use your credit score along with other relevant information provided by you, such as income, work status, and down payment amount. In general, higher scores allow access to more credit at competitive rates.

Insurance carriers can also use credit scores to help assess risk and to accurately price homeowners and automobile insurance policies.

Is Credit Score the Only Thing Used by Lenders for Loan Approval?

No, a credit score is just one part of several factors lenders use in their lending criteria. Other lending criteria considered may include:

- Loan-to-Value Ratio

- Income

- Current employment and work history

Consumers are encouraged to shop for the best loan rates and conditions. Accordingly, the VantageScore® model does not penalize multiple inquiries made within a short period. When several inquiries are made within a shortened timeframe, it is assumed that the consumer is shopping around for a rate and not opening multiple lines of credit.

The VantageScore® model uses a 14-day rolling window in which all credit inquiries within that window are considered one inquiry regardless of the type of account. So regardless of whether the credit inquiry is made in response to a mortgage, auto, or bank credit card application, it will be counted only once during that 14-day window.

There are several ways to improve your credit score. However, it’s much more important to focus on improving what’s in your credit report rather than over your credit score. Here are some quick tips to help:

- Pay Your Bills on Time, Every Month. Payment history is the largest factor in your credit score.

- Apply for Credit Only When You Need It. Try not to open too many accounts too frequently. These frequent inquiries can ding your credit.

- Keep Your Outstanding Balances Low. Keep balances below 30 percent of the credit limit on each of your revolving accounts.

- Reduce Your Total Debt. It is not necessarily bad to have debt as long as it’s manageable. Too much debt at high interest rates can get out of hand if a financial emergency comes up. Consider paying down some of your outstanding loans.

- Build Up Credit History. Maintaining a timely payment history for a mix of accounts (e.g. credit cards, auto, mortgage) over a long period can improve your score.

Five major categories make up a credit score:

40% Payment History

Essentially, lenders want to know whether you’re good about paying your loans on time.

23% Credit Usage

Credit usage, also known as credit utilization, is the ratio between the total credit used and your total credit limit on your revolving accounts. It is best to keep your credit usage below 30%.

21% Credit Age

The average of your oldest open credit accounts to your newest open credit accounts determines your credit age. In general, the longer your credit history the better, particularly accounts with a good payment history and no late payments.

11% Credit Mix

It’s important to have a mix of different types of credit like revolving credit and installment loans. Your score will likely be higher if you have a good payment history with both, installment loans, like student loans and mortgages, and revolving credit, like credit cards.

5% Inquiries

Any time you apply for a credit card, or a lender checks your credit for a loan, it’s known as an inquiry. Hard inquiries show on your credit report when your credit is pulled by a lender for a car loan, mortgage, or credit card. However, soft inquiries don’t show on your credit report and occur when you check your credit, or a lender pre-approves you for an offer.

Applying for several credit cards or opening multiple credit accounts in a short period creates hard inquiries and could signal an increased credit risk to a lender.

Credit reports, also known as credit files, are composed of the credit-related data a credit reporting company has gathered about consumers from different sources. Credit reports include records of mortgage payments, credit card balances, credit card payments, auto loan payments, and credit inquiries. It may also include accounts that have gone into collections, public records, and other information from government sources.

Credit reports include the following about your debt accounts:

- A list of creditors that have extended credit or loans.

- Total loan amounts and credit card limits.

- Payment amount and history on all loans and credit lines.

Credit reports may also include:

- Inquiries, each time your credit report was pulled by a lender in the past 2 years.

- Your current and/or former address(es)

- Your current and/or former employers

- Other details of public record

Under Federal law, you are entitled to receive one free copy of your credit report from each credit reporting agency every 12 months. You can obtain a free copy of your credit reports at https://www.annualcreditreport.com or by calling 1-877-322-8228. For more information visit https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-report-en-309/.

A credit score is a three-digit number calculated to indicate your creditworthiness. The higher the score, the more creditworthy you are to a lender. A credit score is calculated from the information in your credit report and considers your on-time payments, the length of your payment history, your mix of different types of credit accounts, and other such factors. It is important to know that your score does not take your age, income, employment, marital status, or your bank account balances into account.

You can learn more about credit scores and scoring models from the Consumer Financial Consumer Financial Protection Bureau website: https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-score-en-315/

VantageScore® was founded by the 3 leading credit reporting agencies – Experian, Equifax, and TransUnion. This credit score model was developed by a representative team of statisticians, analysts, and credit data experts from each of the credit reporting companies, and is used by hundreds of institutions, including credit unions, banks, credit card issuers, and mortgage lenders.

The VantageScore® 3.0, the score that is shown in SavvyMoney, is a newer and more popular version of VantageScore®. It is calculated on a scale of 300-850, with 300 being the lowest and 850 the highest score.